Exclusively published here at The CFO Magazine on June 15, 2020 https://cfomagazine.com.au/back-to-basics-for-cfos/ Read Time: 3m 30s Back to Basics for CFOs At the core of business success is the fundamentals. Even in a pandemic those businesses that have built a solid working capital base will survive. Those that focused on the basics will come throughContinue reading “Back to Basics for CFOs”

Tag Archives: Cashflow Controls

6 practical steps to introduce advisory services in your firm

The next phase of the accounting industry — where accountants become true advisers to their clients and not just data hoarders — is very much underway. But it’s often difficult to know exactly where to start, and what changes to make to help that transition. Having made that change myself in recent years, with aContinue reading “6 practical steps to introduce advisory services in your firm”

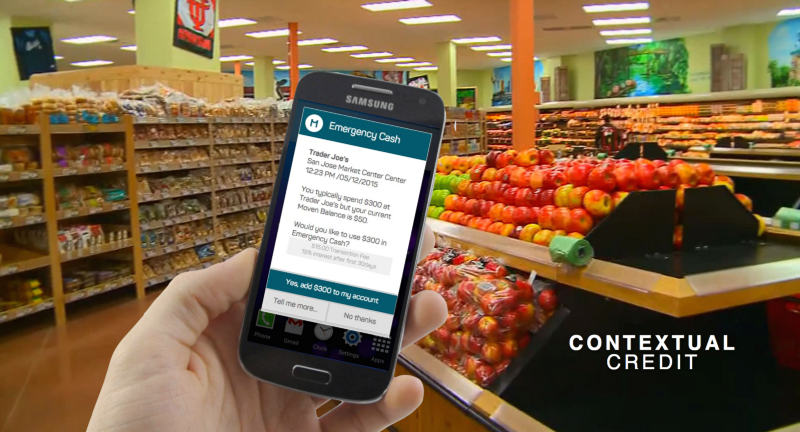

A look into the possible future of banking….it is nothing like we know now

(Picture credit: Moven) I came across this article today by Brett King on Medium. It just proves that the way we think about things and the way we consume things is always going to change in ways that we never thought possible. And it just happens without us even realising it. As I always say, our habitsContinue reading “A look into the possible future of banking….it is nothing like we know now”

The Importance of Credit Control in your Business

Businesses don’t fail because of a lack of profit…they fail because of a lack of cashflow ! Here are 5 simple tips to develop a credit control policy when extending credit to your customers via BRW http://www.brw.com.au/p/leadership/how_to_develop_credit_control_policy_gxoFVWLHxezQe33G51Rj5L

2015 cash flow forecast…have you done yours yet ?

My latest blog post on the EFS website http://efsstrategic.com.au/prepared-2015-financial-year-cash-flow-forecast/

What are your business’ values ….?

As published in the November edition of the Western Sydney Business Access magazine http://westernsydneyaccess.com.au/ Every business has a set of core values underpinning most, if not all of the actions and decisions that its owners and staff make on a daily basis (even if they don’t know what they are). Successful businesses know what theseContinue reading “What are your business’ values ….?”

Risky Business…..

“Article as appeared in the September edition of Western Sydney Business Access…..” SMEs are exposed to risks all the time. Some are risks that are imposed upon them whilst some are risks that they choose take. Such risks can directly affect their day-to-day operations, or their impact may be serious enough for the business toContinue reading “Risky Business…..”